I first met Sean Duffy -- the health entrepreneur, not the US congressman -- at TEDMED 2009. That was the year the founder of TED helped resurrect the medical version of his famed event after a long

>

20 min. Read

1.31.20

The Omada Health Report

In this article:

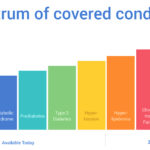

Omada Health is widely expected to go public later this year. In anticipation of the company’s S-1 filing, E&O has put together this 5,200-word report, including year-over-year growth in participants, estimates for annual revenue figures going back to 2015, which medical conditions the company could target next, and much, much more.

×

![]()