The very first long-form report that Exits & Outcomes published was called Approximating Livongo Health's S-1. That was in May 2019. Almost a year later I wrote a similar report about Livongo's biggest rival at the time -- Omada Health. I fully

>

21 min. Read

11.22.24

Approximating Omada Health’s S-1 Before Its 2025 IPO

In this article:

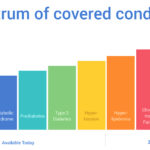

This 5,500-word report includes estimates for Omada Health’s annual revenues (2015-2024), reveals some of its pricing, tracks its customer growth, details its annual net new participants, and examines how GLP-1s have likely driven significant growth for the company in 2024. Plus: Other considerations as an IPO likely nears in 2025.

×

![]()