Less than five years ago, longtime healthcare IT executive Glen Tullman took the stage at TechCrunch Disrupt 2014 and announced the launch of his new startup, a diabetes-focused company called

5.01.19

14 min. Read

Approximating Livongo Health’s S-1

In this article:

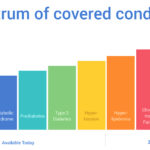

Digital health company Livongo Health is expected to go public later this year. In anticipation of the company’s S-1 filing, E&O has put together this 3,600-word report, including annual revenue figures, quarterly adoption metrics, regulatory mishaps, acquisitions, growth strategies, predictions and much, much more.

×

![]()